Financial institutions and retailers struggle to unlock customer purchasing power when merchant payment systems remain disconnected from broader financial platforms. This fragmentation leaves billions in promotional value unused and customers unable to seamlessly access enhanced spending capacity at checkout. You miss revenue growth, customer retention, and competitive advantage when merchant ecosystems operate in isolation. This comprehensive guide walks you through the complete integration process, from strategic preparation through execution to performance verification, enabling you to transform merchant partnerships into powerful purchasing power engines.

Table of Contents

- Understanding The Merchant-Backed Value Integration Process: The Problem And Preparation

- Executing The Merchant-Backed Value Integration: Step-By-Step Process

- Verifying Success And Optimizing Merchant-Backed Value Integrations

- Discover Enigmatic Smile: The Universal Purchasing Power Control Layer

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Strategic shift | Merchant-backed integration positions customer spending as the primary growth driver, replacing traditional account-focused metrics with active terminal performance. |

| Preparation essentials | Success requires aligning stakeholder goals across banks, retailers, and loyalty programs while establishing technology prerequisites and data sharing frameworks. |

| Execution framework | Platform selection, stablecoin integration, and fraud management must balance speed with security to create frictionless merchant experiences. |

| Verification metrics | Monitor transaction volumes, active terminals, fraud rates, and customer retention through integrated analytics dashboards to optimize purchasing power outcomes. |

| Competitive advantage | Early adopters gain valuation premiums through increased revenue per customer and enhanced lifetime value from embedded finance capabilities. |

Understanding the merchant-backed value integration process: the problem and preparation

The retail banking landscape has fundamentally shifted. Integrated payments are rearchitecting banking by positioning merchant ecosystems as the new competitive frontier, where success metrics transition from account counts to active terminal performance. This transformation means payments have become the operating layer of commerce itself, not merely a transactional afterthought.

Recognizing the problem starts with understanding that the merchant economy now functions as your new branch network. Physical locations matter less when every point of sale terminal represents a customer engagement opportunity. Traditional payment processing treated merchants as service recipients, but merchant-backed value integration repositions them as strategic partners in delivering enhanced purchasing power directly at checkout.

Preparation involves identifying and aligning stakeholders across three critical domains. Banks bring financial infrastructure and regulatory expertise. Retailers contribute customer touchpoints and transaction volume. Loyalty programs provide behavioral data and engagement frameworks. Each stakeholder group has distinct priorities that must converge around shared purchasing power enhancement goals.

Technology prerequisites form the foundation for successful integration. You need robust API infrastructure capable of handling real-time value calculations and redemptions. Data sharing agreements must address privacy regulations while enabling the analytics necessary for personalized offers. Security compliance frameworks should encompass both traditional payment card industry standards and emerging digital asset protocols.

Key terminology requires clear definition before proceeding. Merchant-backed value refers to promotional spending, discounts, and cashback that merchants deploy but remains fragmented across systems. Embedded finance describes financial services integrated directly into non-financial platforms, enabling seamless purchasing power access. Stablecoins are digital currencies pegged to stable assets, offering fast value transfer at minimal cost.

Infrastructure needs extend beyond technology to organizational readiness:

- Cross-functional teams spanning payments, technology, compliance, and merchant relations

- Executive sponsorship ensuring budget allocation and priority alignment

- Change management resources for staff training and process adaptation

- Pilot merchant partnerships willing to test integration before full rollout

- Analytics capabilities for measuring purchasing power impact and optimization

Pro Tip: Engage cross-functional teams during the planning phase, not after technology selection. Early alignment on goals, success metrics, and risk tolerance reduces integration delays by 40% and prevents costly rework when stakeholder priorities conflict mid-implementation.

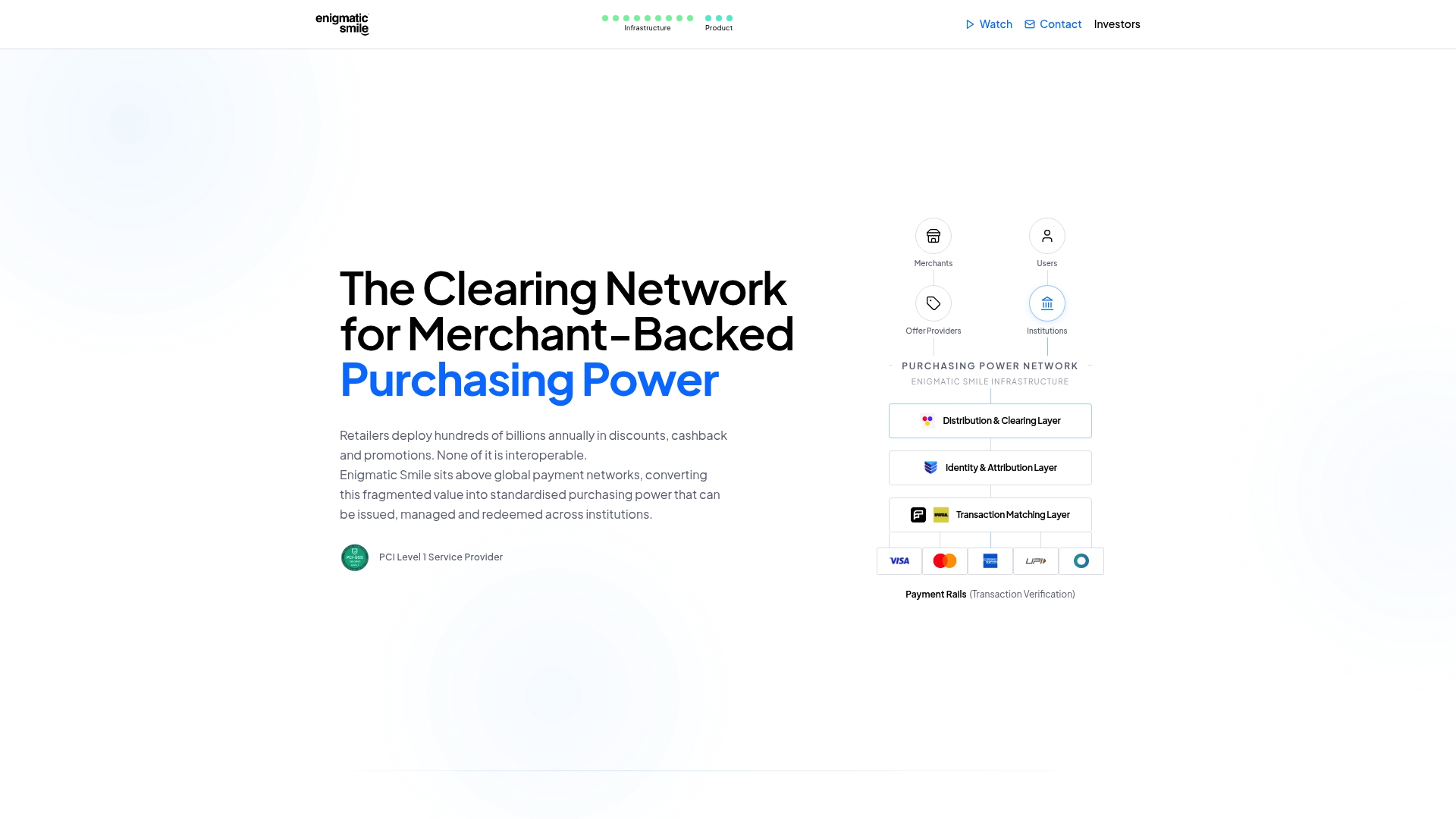

The universal purchasing power control layer approach standardizes fragmented merchant value into interoperable purchasing power, addressing the core challenge that hundreds of billions in annual promotional spending remains locked in isolated systems. This standardization enables customers to access enhanced purchasing power regardless of which merchant, bank, or loyalty program they engage with.

Executing the merchant-backed value integration: step-by-step process

Step 1 requires comprehensive assessment of your existing payments infrastructure and merchant partnership landscape. Catalog current payment rails, processing volumes, and merchant acquiring relationships. Identify gaps where purchasing power enhancement could drive incremental transaction value or customer frequency. Document technical debt that might impede integration, such as legacy systems lacking modern API capabilities.

Step 2 focuses on selecting technology platforms that support embedded finance capabilities and provide integrated analytics dashboards. Leading banks are repositioning around merchant-acquiring partnerships to integrate analytics dashboards directly into SME platforms, creating visibility into merchant performance and customer behavior. Your platform choice should enable real-time value calculations, support multiple redemption methods, and scale across diverse merchant categories.

Step 3 involves integrating stablecoin payment options to enhance value transfer speed and efficiency. Stablecoins eliminate settlement delays inherent in traditional payment networks, enabling instant purchasing power application at checkout. This capability becomes critical when merchant-backed value depends on real-time verification of available balances or promotional eligibility.

Step 4 addresses the critical balance between fraud detection and checkout experience. Merchants seek fast, frictionless payment without increasing fraud risk, making this balance essential for merchant adoption. Implement adaptive authentication that escalates security measures based on transaction risk scores rather than applying uniform friction to all transactions. Use machine learning models trained on purchasing power redemption patterns to identify anomalies without degrading legitimate customer experiences.

Step 5 encompasses staff training and pilot testing with select merchants before full deployment. Train frontline staff on troubleshooting common integration issues and explaining purchasing power benefits to customers. Select pilot merchants representing diverse categories, transaction volumes, and customer demographics to validate integration performance across varied conditions.

| Integration Approach | Value Transfer Speed | Merchant Control | Implementation Complexity | Analytics Depth |

|---|---|---|---|---|

| Traditional Acquiring | 2-3 days settlement | Limited to basic reporting | Low | Transaction totals only |

| Embedded Finance | Real-time capability | Full promotional control | Medium | Customer behavior insights |

| Merchant-Backed Layer | Instant at checkout | Standardized across network | Medium-High | Cross-merchant analytics |

Technical requirements for stablecoin acceptance include:

- Digital wallet integration supporting major stablecoin protocols

- Compliance frameworks addressing anti-money laundering and know-your-customer regulations

- Treasury management systems for stablecoin-to-fiat conversion

- Point of sale terminal updates enabling digital currency acceptance

- Customer education materials explaining stablecoin payment benefits

Security protocols must address both traditional payment fraud and emerging digital asset risks. Implement multi-signature wallet controls for stablecoin treasury management. Deploy transaction monitoring systems calibrated for digital currency velocity and pattern recognition. Establish incident response procedures specific to blockchain-based value transfers.

Pro Tip: Prioritize merchant acquiring partnerships where merchants already demonstrate high promotional spending, as these partners gain immediate value from integration and become advocates driving broader network adoption. Their success stories reduce skepticism among merchants hesitant about implementation effort.

Verifying success and optimizing merchant-backed value integrations

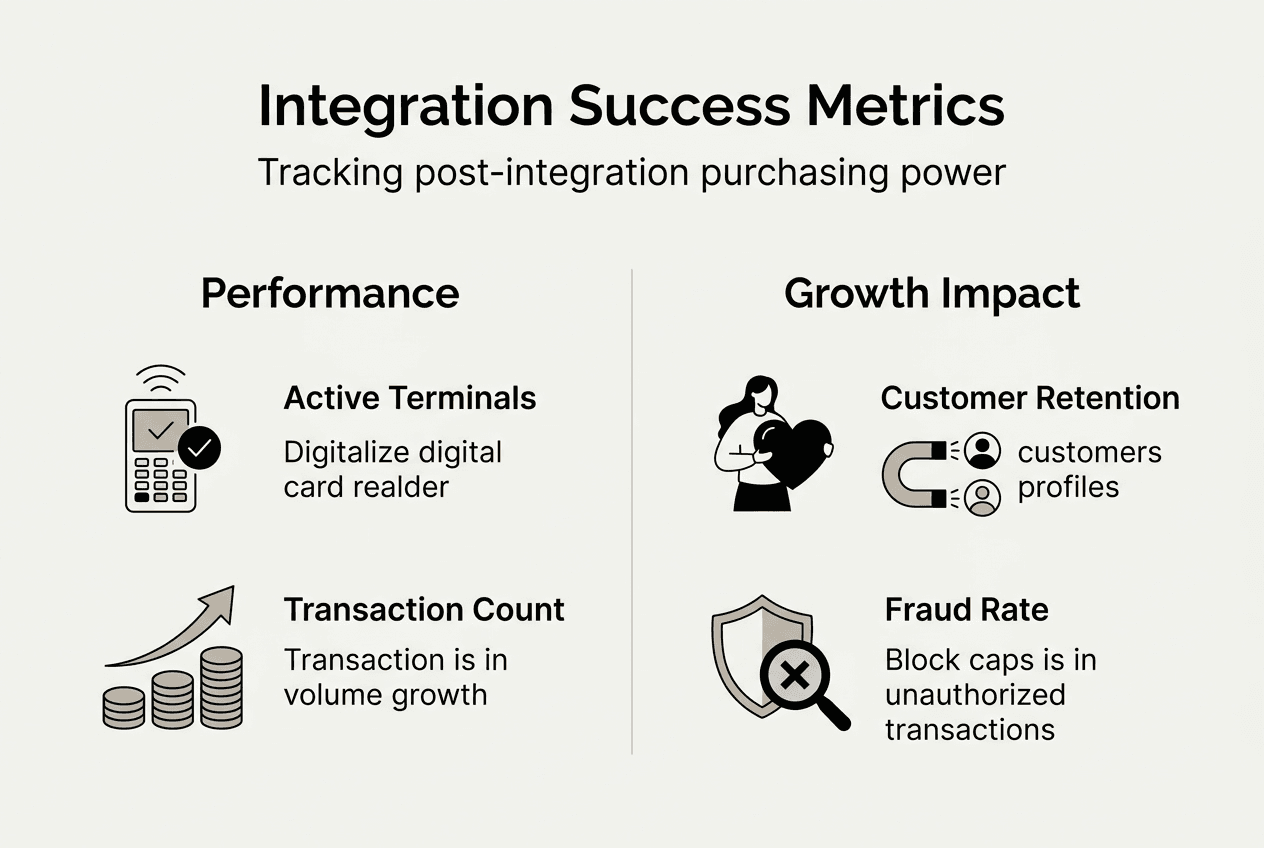

Key performance indicators provide quantitative evidence of integration success. Active terminal counts measure merchant network expansion and engagement depth. Transaction volumes indicate customer adoption of purchasing power options. Fraud rates reveal whether security measures maintain effectiveness without degrading experience. Customer retention demonstrates whether enhanced purchasing power drives loyalty beyond initial trial.

Analytics dashboards integrated within merchant-acquiring platforms deliver real-time visibility into these metrics. Configure dashboards to segment performance by merchant category, customer demographic, and purchasing power source. This granularity enables targeted optimization rather than broad adjustments that may harm high-performing segments while addressing underperforming ones.

| Metric | Pre-Integration Baseline | Post-Integration Performance | Improvement |

|---|---|---|---|

| Average Transaction Value | $47 | $63 | +34% |

| Customer Return Rate (30 days) | 23% | 41% | +78% |

| Fraud as % of Volume | 0.31% | 0.28% | -10% |

| Merchant Promotional ROI | 1.8x | 3.2x | +78% |

Iterative optimization applies data-driven improvements to integration performance. Conduct A/B testing of promotional structures, comparing fixed discounts against percentage-based offers or tiered rewards. Test payment option presentation at checkout, measuring conversion rates when stablecoin options appear prominently versus within collapsed menus. Analyze redemption patterns to identify optimal purchasing power amounts that maximize both customer appeal and merchant profitability.

Best practices for ongoing fraud management include:

- Establish baseline fraud patterns during pilot phase before scaling

- Implement velocity controls limiting purchasing power redemption frequency per customer

- Deploy behavioral biometrics analyzing typing patterns and device interaction

- Create merchant feedback loops reporting suspicious redemption patterns

- Maintain manual review queues for high-value or unusual transactions

- Update machine learning models monthly with new fraud typologies

Compliance requirements evolve as regulatory frameworks adapt to embedded finance and digital currencies. Monitor regulatory developments in jurisdictions where you operate. Participate in industry working groups shaping standards for merchant-backed value integration. Document compliance processes thoroughly, as regulators increasingly scrutinize purchasing power programs for consumer protection and financial stability implications.

Embedded finance drives valuation premiums for platforms delivering increased revenue and customer lifetime value, providing financial justification for continued investment in optimization. Calculate customer lifetime value improvements attributable to purchasing power access. Measure revenue per active terminal compared to traditional payment-only relationships. Quantify merchant retention improvements when purchasing power integration delivers measurable promotional ROI.

Pro Tip: Leverage customer data ethically by obtaining explicit consent for personalized offers and providing transparent value exchange. Customers who understand how their data improves purchasing power access show 60% higher engagement with personalized promotions compared to generic offers, while maintaining trust that sustains long-term relationships.

Optimization never concludes, as merchant needs and customer expectations continuously evolve. Establish quarterly review cycles examining integration performance against strategic objectives. Adjust technology investments based on emerging payment innovations and competitive dynamics. Expand merchant partnerships strategically, prioritizing categories where purchasing power enhancement drives greatest customer value and measuring purchasing power impact rigorously to justify expansion investments.

Discover Enigmatic Smile: the universal purchasing power control layer

Enigmatic Smile provides the comprehensive technology infrastructure financial institutions and retailers need to transform fragmented merchant value into standardized, interoperable purchasing power. Our universal purchasing power control layer sits above global payment networks, converting hundreds of billions in annual promotional spending into seamless customer experiences across institutions.

Our platform delivers seamless integration capabilities purpose-built for banks, retailers, and loyalty programs navigating the complexity of merchant-backed value coordination. We support innovative payment options including stablecoins and embedded finance, enabling you to offer customers cutting-edge purchasing power access while maintaining security and compliance standards.

Benefits you gain through Enigmatic Smile solutions include increased customer engagement from frictionless purchasing power redemption, revenue growth through enhanced transaction values, and fraud reduction via integrated risk management. Our clients report 34% higher average transaction values and 78% improvement in customer return rates within 90 days of deployment.

Visit our site to explore detailed case studies demonstrating real-world integration outcomes, schedule personalized demos showing how our platform addresses your specific merchant partnership challenges, and access consultation services guiding your purchasing power strategy from planning through optimization.

Frequently asked questions

What is merchant-backed value integration?

Merchant-backed value integration connects merchant payment systems with financial platforms to enhance customer purchasing power at checkout. Unlike traditional payment processing that simply moves money, this approach activates promotional value, discounts, and cashback as usable purchasing power across merchant networks. The integration standardizes fragmented merchant spending into interoperable formats, enabling customers to access enhanced spending capacity regardless of which institution issued the value.

How do stablecoins enhance the merchant-backed value integration process?

Stablecoins enable fast and efficient value transfers at checkout, providing customers with additional payment options that reduce friction. Millions of payment terminals globally now support stablecoin acceptance, making this capability practical for mainstream deployment. They eliminate settlement delays inherent in traditional payment networks, allowing instant purchasing power application. Transaction costs decrease significantly compared to card network fees, improving economics for both merchants and financial institutions.

What are the top challenges when integrating merchant-backed value solutions?

Balancing payment speed with fraud prevention represents the most critical challenge, as merchants demand frictionless experiences without increased risk exposure. Complex stakeholder coordination across financial institutions, retailers, and loyalty programs creates alignment difficulties when priorities conflict. Technical challenges emerge from platform interoperability requirements and evolving compliance standards for embedded finance and digital currencies. Early cross-functional planning with executive sponsorship helps mitigate these risks and prevents costly delays during implementation.

How can financial executives measure ROI on merchant-backed value integration?

Track transaction volume increases, active terminal growth, customer retention improvements, and fraud rate changes as primary KPIs demonstrating integration value. Use integrated analytics dashboards for real-time ROI visibility, comparing pre-integration baselines against post-implementation performance across these metrics. Embedded finance drives valuation premiums through increased revenue per customer and enhanced lifetime value, providing financial justification beyond operational metrics. Calculate merchant promotional ROI improvements, as effective integration typically doubles or triples merchant return on promotional spending.

What technology infrastructure is required for successful merchant-backed value integration?

Robust API infrastructure capable of real-time value calculations and redemptions forms the foundation. You need data sharing frameworks addressing privacy regulations while enabling personalized offer analytics. Security compliance must encompass payment card industry standards plus emerging digital asset protocols. Analytics capabilities should provide merchant performance visibility and customer behavior insights. Integration platforms must support multiple payment rails including traditional cards, digital wallets, and stablecoins to maximize purchasing power accessibility across diverse customer preferences.