Payment networks generated $2.4 trillion in global revenue as of 2023, yet most financial decision-makers still view these systems as commoditized infrastructure rather than strategic assets. This misconception leaves enormous value on the table. In 2026, the landscape has shifted dramatically. Consumers now strategically combine multiple payment methods to maximize rewards, while merchants invest heavily in premium solutions to drive growth. Interoperable networks that convert fragmented merchant rewards into standardized purchasing power are no longer experimental, they are essential. This article explains why investing in innovative payment networks delivers measurable benefits: reduced transaction costs, faster settlements, enhanced fraud protection, and the ability to participate in emerging machine-native payment protocols that power the AI economy.

Table of Contents

- The Evolving Payment Landscape And Market Opportunity

- How Interoperability Transforms Payment Networks

- Innovative Protocols Driving Payment Network Evolution

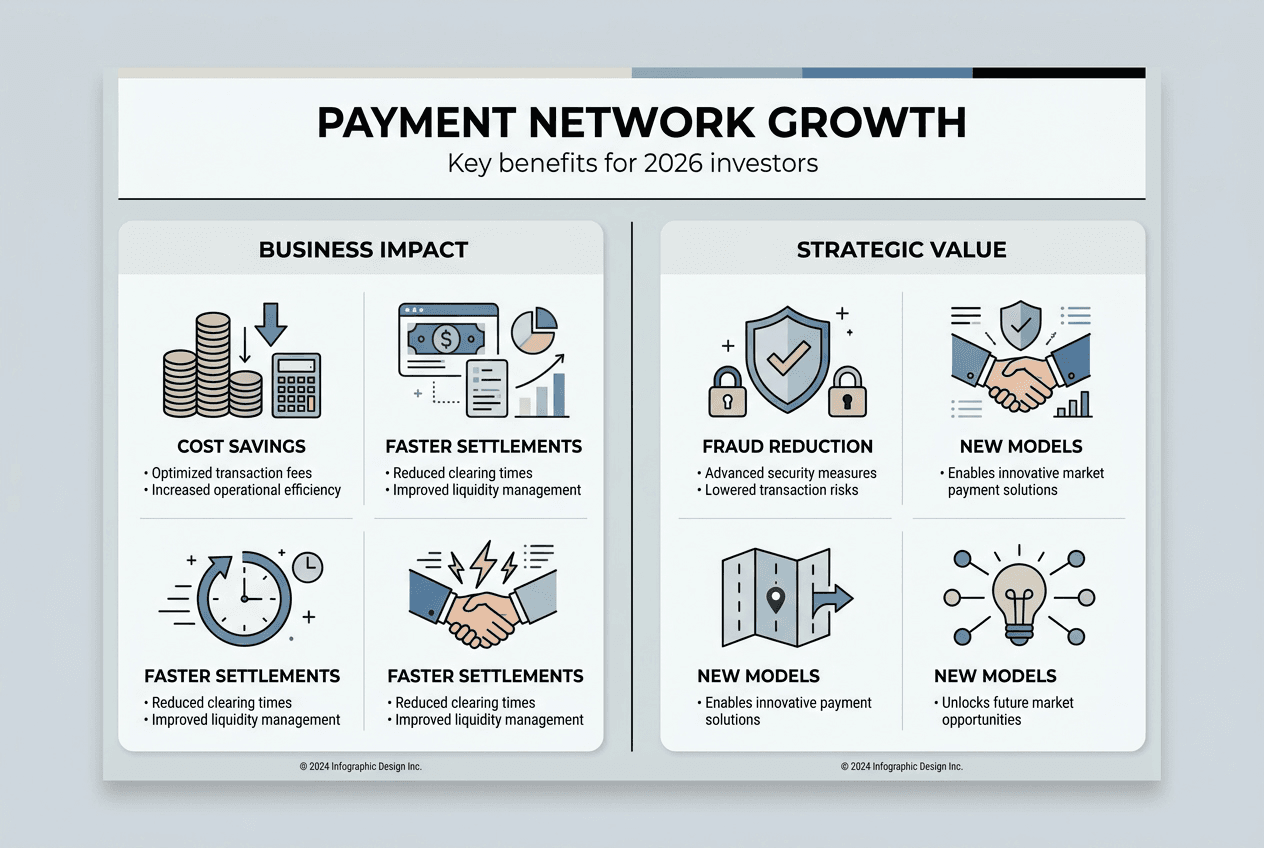

- Strategic Benefits Of Investing In Payment Networks For Retailers And Merchants

- Explore Innovative Payment Solutions With Enigmatic Smile

Key takeaways

| Point | Details |

|---|---|

| Market size | Payment networks represent a $2.4 trillion revenue opportunity globally as of 2023. |

| Efficiency gains | Interoperable systems reduce transaction costs by 10-15% and processing times by up to 25%. |

| Settlement speed | Cross-border settlements can drop from days to under 20 minutes with modern infrastructure. |

| Consumer adoption | 23% of consumers use Buy Now Pay Later, while 37% increase debit card usage to avoid debt. |

| Future protocols | Innovations like x402 enable gasless micropayments for AI services with near-zero fees. |

The evolving payment landscape and market opportunity

Global payment revenues reached $2.4 trillion in 2023, a figure that reflects the explosive growth of digital commerce, cross-border transactions, and diversified payment methods. This massive market is far from static. Consumer behaviors are evolving rapidly, with 23% now using Buy Now Pay Later services for everyday purchases, while 37% of U.S. consumers actively increase debit card usage to avoid accumulating debt. These shifts signal a fundamental change in how people think about payment instruments: not as passive tools, but as strategic levers for managing cash flow, earning rewards, and controlling spending.

Small and medium-sized businesses are equally proactive. Roughly 89% of SMBs invest in premium payment solutions specifically to accelerate growth and improve operational efficiency. They recognize that payment infrastructure is not a back-office function but a competitive differentiator. Faster settlements mean better cash flow. Lower transaction fees mean higher margins. Integrated loyalty and rewards programs mean stronger customer retention. The payment landscape in 2026 is defined by this strategic mindset, where every transaction is an opportunity to capture value.

For financial decision-makers evaluating investment opportunities, this context is critical. The payment networks that win in this environment are those that support seamless integration across multiple methods, enabling faster settlements and reducing friction at every step. Networks that remain siloed or fail to offer interoperability will struggle to compete as consumers and merchants demand more flexibility and control.

Consider the broader implications. Payment networks are no longer just rails for moving money. They are platforms for distributing purchasing power, managing merchant-backed rewards, and enabling entirely new commerce models. The $2.4 trillion market is not a ceiling but a foundation. As AI-driven services, machine-to-machine transactions, and real-time settlement systems mature, the addressable market will expand exponentially. Investing in payment networks now means positioning for this next wave of growth, not just capturing today's revenue streams.

How interoperability transforms payment networks

Interoperability is the single most impactful innovation in modern payment infrastructure. Traditional networks operate in silos, each with proprietary standards, settlement processes, and fee structures. This fragmentation creates inefficiencies that cascade through the entire value chain. Interoperable payment networks reduce transaction costs by 10-15% and processing times by up to 25%, according to research from the Bank for International Settlements. These are not marginal improvements. They represent fundamental shifts in how value moves through the financial system.

The most dramatic gains appear in cross-border settlements. Legacy systems typically require T+2 settlement windows, meaning transactions take two business days to finalize. During this period, capital is locked, counterparty risk persists, and currency fluctuations can erode value. A top-20 payments company cut cross-border settlement time by 90%, reducing the window from days to under 20 minutes. This transformation unlocks working capital, eliminates unnecessary hedging costs, and enables real-time liquidity management for merchants and financial institutions.

The table below contrasts traditional payment networks with interoperable systems across key performance dimensions:

| Metric | Traditional Networks | Interoperable Networks |

|---|---|---|

| Transaction cost | 2-3% per transaction | 0.5-1% per transaction |

| Settlement time | T+2 (48+ hours) | T+0 (under 20 minutes) |

| Cross-border complexity | High (multiple intermediaries) | Low (direct settlement paths) |

| Fraud risk | Moderate to high | Low (real-time verification) |

| Integration effort | Months per new partner | Weeks via standardized APIs |

Pro Tip: Prioritize payment network investments that support ISO 20022 messaging standards and permissioned zero-knowledge rollups for scalability. These technologies provide the foundation for seamless interoperability and future-proof your infrastructure as transaction volumes grow.

Interoperability also reduces technical debt. When networks speak a common language, integrating new payment methods, currencies, or partners becomes exponentially easier. Instead of building bespoke connections for each relationship, institutions can leverage standardized protocols that work across the ecosystem. This accelerates time to market for new products and reduces the engineering burden on internal teams. For financial decision-makers, this translates to lower operational costs and faster innovation cycles.

The strategic value extends beyond cost and speed. Interoperable networks enable entirely new business models, such as cross-border settlements that combine multiple currencies, payment methods, and reward systems in a single transaction. Merchants can offer customers the ability to pay with a mix of loyalty points, stablecoins, and traditional currency, all settled in real time. This flexibility drives conversion rates and customer satisfaction, creating competitive advantages that are difficult to replicate with legacy infrastructure.

Innovative protocols driving payment network evolution

Emerging payment protocols are redefining what is possible in digital commerce, particularly for machine-to-machine transactions and AI-driven services. The most notable innovation is x402, which activates the HTTP 402 Payment Required code to enable frictionless, protocol-native, stablecoin micropayments. This protocol addresses a critical gap in the current payment ecosystem: the inability to monetize low-value, high-frequency transactions without prohibitive overhead.

Traditional payment flows introduce multiple points of friction. Credit card networks charge 2-3% per transaction, making micropayments economically unviable. Subscription models force customers into all-or-nothing commitments, creating barriers to entry for casual users. Paywalls require manual authentication, adding latency and abandonment risk. These limitations are tolerable for high-value transactions but catastrophic for the AI economy, where services are consumed in tiny increments across millions of automated interactions.

x402 eliminates these barriers by embedding payment logic directly into the HTTP protocol. When a client requests a resource, the server responds with a 402 status code and payment instructions. The client automatically executes the payment using stablecoins like USDC, with near-zero fees and sub-second settlement. No manual intervention, no subscription overhead, no fraud risk. The protocol supports gasless transactions, meaning users do not need to hold native blockchain tokens to pay fees, removing yet another layer of complexity.

For developers building AI services, x402 offers several compelling advantages:

- Automatic monetization without building custom payment infrastructure

- Sub-cent micropayments with economically viable fee structures

- Real-time settlement that eliminates accounts receivable and cash flow delays

- Protocol-level security that reduces fraud and chargebacks to near zero

- Seamless integration with existing HTTP-based APIs and services

The strategic implications are profound. Without protocol-native payments, AI's growth risks systemic revenue collapse due to legacy paywalls and subscriptions that cannot scale to the volume and granularity of machine-to-machine commerce. As AI agents increasingly act as autonomous economic actors, consuming and providing services in real time, the payment infrastructure must evolve to match this new reality. x402 and similar protocols represent the foundation for this next generation of commerce.

Beyond AI, these protocols unlock opportunities in IoT, content monetization, and usage-based pricing models. Imagine a smart city where vehicles automatically pay for parking, tolls, and charging in real time, with no human intervention. Or a content platform where readers pay per article consumed, with payments settled instantly and creators receiving funds within seconds. These scenarios are not theoretical. They are being built today on modern payment technology that prioritizes interoperability, low latency, and minimal friction.

"The future of payments is not about replacing credit cards or bank transfers. It is about creating entirely new transaction types that were previously impossible due to cost, latency, or complexity. Protocol-native payments make this future tangible."

Strategic benefits of investing in payment networks for retailers and merchants

For retailers and merchants, investing in innovative payment networks delivers measurable improvements across multiple dimensions: fraud reduction, cost savings, customer satisfaction, and competitive positioning. Start with fraud. U.S. consumers reported $12.5 billion in fraud losses in 2024, a figure that continues to climb as attack vectors become more sophisticated. Modern payment networks with real-time verification, tokenization, and machine learning-based anomaly detection reduce fraud risk substantially, protecting both merchants and customers from losses.

Cost savings are equally significant. EthSwitch IPS reduces transaction costs by about 47%, making payments more affordable for merchants operating on thin margins. Lower transaction costs translate directly to higher profitability, enabling merchants to reinvest savings into growth initiatives, customer acquisition, or enhanced rewards programs. When combined with faster settlement times, these savings also improve working capital management, reducing the need for expensive short-term financing.

Customer purchasing power is another critical benefit. Interoperable payment networks allow merchants to offer flexible payment options, from traditional cards to Buy Now Pay Later, stablecoins, and loyalty point redemption. Customers can choose the method that maximizes their rewards or aligns with their cash flow preferences. This flexibility increases conversion rates and average order values, as customers feel empowered to make purchases they might otherwise defer.

The table below summarizes key metrics comparing traditional and innovative payment networks:

| Metric | Traditional Networks | Innovative Networks |

|---|---|---|

| Annual fraud losses | $12.5B (U.S. 2024) | Reduced by 60-80% |

| Transaction cost | 2-3% | 0.5-1.5% |

| Settlement time | 2-3 days | Real-time to 20 minutes |

| Payment method diversity | Limited (2-3 options) | High (5+ integrated options) |

| Merchant reward flexibility | Low (siloed programs) | High (interoperable rewards) |

Pro Tip: When evaluating payment networks, prioritize those with demonstrated capability to integrate diverse payment methods and comply with upcoming regulatory standards like ISO 20022 and MiCA in Europe. Regulatory alignment reduces future compliance costs and ensures long-term viability.

Beyond operational metrics, innovative payment networks enable strategic differentiation. Merchants who offer superior payment experiences, faster checkouts, and seamless reward redemption build stronger customer loyalty and brand equity. In competitive markets, these advantages drive repeat purchases and word-of-mouth referrals, creating compounding value over time.

Investing in payment networks also positions merchants to participate in emerging commerce models. As machine-to-machine payments, AI-driven transactions, and real-time settlement become standard, merchants with modern infrastructure will capture disproportionate share of this growth. Those relying on legacy systems will face increasing costs, slower innovation cycles, and competitive disadvantages that are difficult to overcome. The strategic window to invest is now, before the gap between leaders and laggards becomes insurmountable.

Finally, consider the broader ecosystem benefits. Innovative payment networks facilitate purchasing power control by converting fragmented merchant rewards, discounts, and promotions into standardized units that can be issued, managed, and redeemed across institutions. This interoperability unlocks hundreds of billions in value currently trapped in siloed loyalty programs, creating new revenue streams and deeper customer engagement.

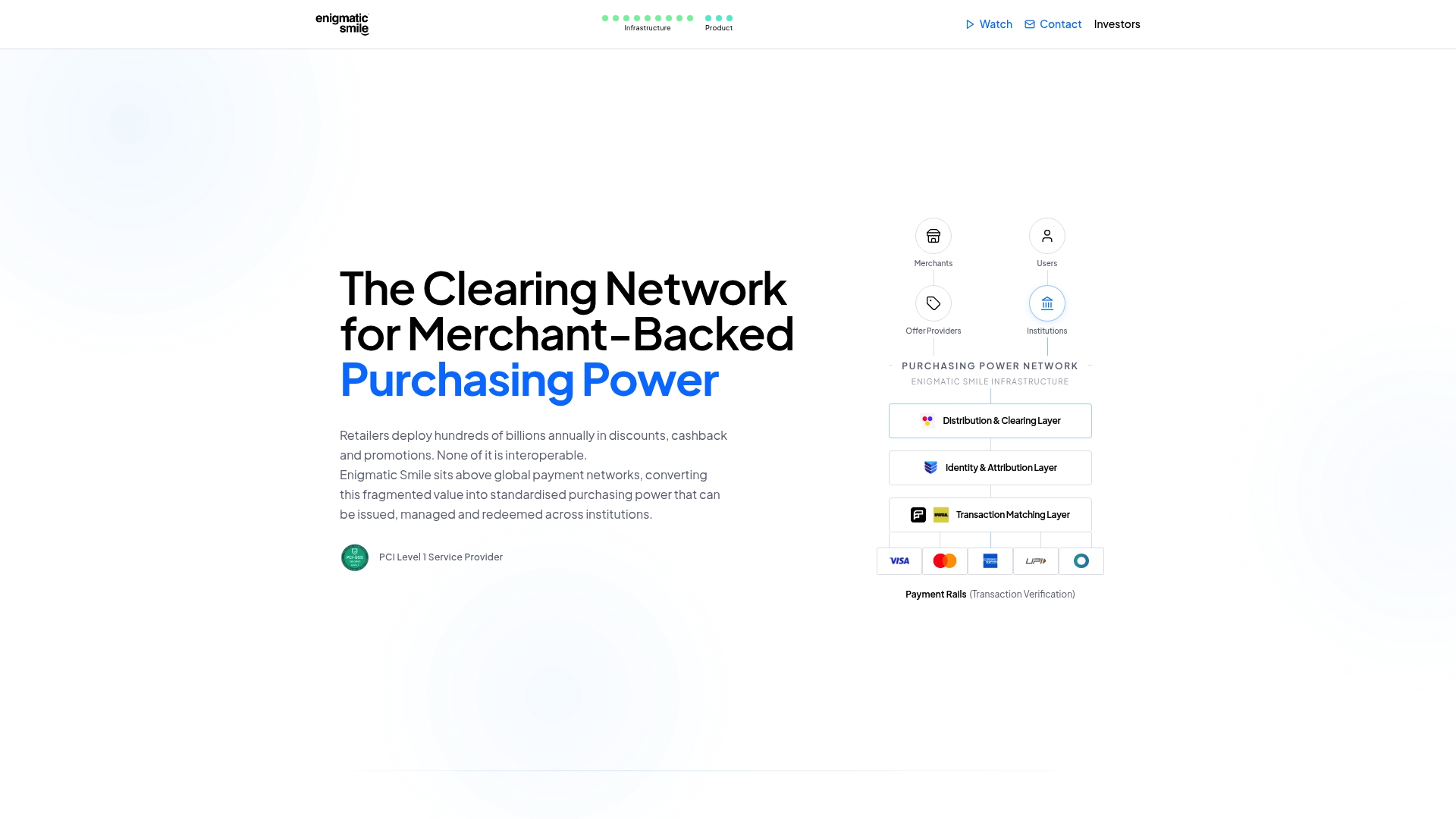

Explore innovative payment solutions with Enigmatic Smile

Retailers deploy hundreds of billions annually in discounts, cashback, and promotions, yet none of this value is interoperable. Enigmatic Smile addresses this fragmentation by providing a universal purchasing power control layer that sits above global payment networks. The platform converts merchant-backed rewards into standardized purchasing power that can be issued, managed, and redeemed across institutions, accelerating settlements and enhancing payment interoperability.

The platform supports seamless integration with multiple payment standards, including ISO 20022 and emerging protocols like x402, making it ideal for financial decision-makers aiming to unlock customer rewards and operational efficiencies. Whether you are evaluating investment opportunities in payment infrastructure or seeking to implement cutting-edge technology for your retail operations, Enigmatic Smile offers the tools and expertise to realize measurable benefits. Visit Universal purchasing power solutions to explore how this innovative clearing network can transform your payment strategy and position your organization for growth in 2026 and beyond.

Frequently asked questions

What are the main advantages of interoperable payment networks?

Interoperable networks reduce transaction costs by 10-15% and processing times by up to 25%, according to Bank for International Settlements research. They enable seamless cross-border payments, support diverse payment methods, and lower fraud risk through real-time verification. These advantages translate to better cash flow, higher margins, and improved customer satisfaction for merchants.

How do innovative payment networks enhance consumer purchasing power?

Innovative networks allow consumers to strategically combine payment methods, such as loyalty points, Buy Now Pay Later, and traditional cards, within a single transaction. This flexibility maximizes rewards and aligns with individual cash flow preferences. Interoperable systems also enable redemption of merchant-backed rewards across multiple institutions, unlocking value previously trapped in siloed programs.

What is x402 and why does it matter for AI-driven commerce?

x402 is a protocol that activates the HTTP 402 Payment Required code to enable automatic, gasless micropayments using stablecoins. It allows AI services to monetize usage in real time with near-zero fees and sub-second settlement. This innovation is critical for the AI economy, where legacy paywalls and subscriptions cannot scale to the volume and granularity of machine-to-machine transactions.

How do modern payment networks reduce fraud risk?

Modern networks use real-time verification, tokenization, and machine learning-based anomaly detection to identify and block fraudulent transactions before they complete. These technologies reduce fraud losses by 60-80% compared to traditional systems. Faster settlement times also minimize exposure windows, further lowering risk for both merchants and consumers.

Why should financial decision-makers invest in payment networks now?

The payment landscape is undergoing rapid transformation, with interoperable networks, protocol-native payments, and real-time settlement becoming standard expectations. Investing now positions organizations to capture growth in the $2.4 trillion market, participate in emerging AI and machine-to-machine commerce, and avoid the competitive disadvantages of relying on legacy infrastructure. The strategic window to invest is closing as leaders pull ahead.