Merchant reward programs have become a double-edged sword for financial institutions. While retailers deploy hundreds of billions annually in discounts and cashback, the fragmented nature of these programs creates significant operational headaches and customer confusion. Banks and loyalty program managers face mounting pressure to streamline reward delivery while improving engagement metrics. Standardization offers a clear path forward, transforming scattered promotional value into interoperable purchasing power that works seamlessly across merchants and institutions. The financial benefits are substantial, but understanding how to navigate this shift requires examining both the challenges of current systems and the proven advantages of unified reward frameworks.

Table of Contents

- The Challenges Of Non-Standardized Merchant Rewards

- How Standardization Boosts Efficiency And Scalability

- The Financial Benefits And ROI Of Standardized Programs

- Navigating Regulatory Pressures And Industry Nuances

- Explore Solutions For Standardized Merchant Rewards

- Frequently Asked Questions About Standardizing Merchant Rewards

Key takeaways

| Point | Details |

|---|---|

| Efficiency gains | Standardized systems reduce manual management costs and enable real-time settlement across merchants. |

| Financial returns | Programs achieve 3x to 10x ROI with payback periods of 6 to 18 months. |

| Regulatory compliance | New interchange rules and settlement changes make standardization necessary for cost control. |

| Customer engagement | Unified reward experiences reduce confusion and boost retention by 5 to 20%. |

The challenges of non-standardized merchant rewards

Financial professionals managing merchant reward programs face a landscape cluttered with incompatible systems and disjointed customer experiences. The average consumer now enrolls in 18 loyalty programs, yet this proliferation creates more confusion than value. When rewards cannot transfer between merchants or integrate with existing banking relationships, customers disengage rapidly. The data reveals a stark reality: 77% of traditional programs fail within two years, largely due to fragmentation that prevents meaningful customer engagement.

The operational burden of managing non-standardized rewards extends far beyond customer confusion. Banks and program managers must maintain separate integrations for each merchant partner, manually reconcile transactions across different systems, and troubleshoot redemption failures that arise from incompatible reward formats. This fragmentation inflates operational costs while delaying reward delivery, sometimes by days or weeks. When customers cannot access their earned benefits quickly, trust erodes and program participation drops.

Three critical pain points emerge from fragmented reward systems:

- Manual reconciliation processes consume significant staff time and introduce errors that frustrate both merchants and customers.

- Delayed settlement cycles prevent real-time reward application, reducing the psychological impact of immediate gratification.

- Incompatible data formats across merchants make it impossible to analyze program performance holistically or optimize reward strategies.

The impact on customer behavior is measurable and concerning. When rewards feel complicated or inaccessible, customers simply stop participating. Program managers report that non-standardized systems generate higher support costs, lower redemption rates, and weaker brand loyalty. The universal purchasing power control layer concept addresses these issues by creating a common framework that merchants and institutions can plug into, eliminating the need for custom integrations.

"Fragmented reward programs create operational silos that prevent banks from delivering the seamless, modern experiences customers expect from their financial relationships."

The financial toll extends beyond operational inefficiency. When reward programs fail to engage customers, the entire investment in program development and merchant partnerships delivers minimal return. Banks lose competitive advantage while merchants see no meaningful lift in customer frequency or basket size. This lose-lose scenario drives the urgent need for standardization across the industry.

How standardization boosts efficiency and scalability

Standardized reward systems transform backend operations through unified API layers that create consistency across all merchant touchpoints. Instead of building custom integrations for each partner, financial institutions connect once to a standardized framework that handles reward issuance, tracking, and redemption automatically. This architectural shift eliminates duplicate effort and ensures customers receive identical experiences whether shopping online, in-store, or through mobile apps. The unified APIs enable interoperability that makes scaling to hundreds or thousands of merchant partners feasible without proportional increases in technical resources.

Automation represents the second major efficiency gain from standardization. When reward rules, eligibility criteria, and redemption processes follow common formats, systems can process transactions without human intervention. Campaign managers set parameters once, and the standardized platform applies them consistently across all participating merchants. This automation reduces errors that plague manual systems, where miscommunication between banks and merchants often leads to incorrect reward calculations or failed redemptions. The time savings allow program managers to focus on strategy and optimization rather than troubleshooting individual transactions.

Real-time settlement capabilities emerge naturally from standardized systems. Traditional reward programs often involve complex multi-party transactions where banks, payment networks, and merchants must reconcile balances days or weeks after purchases occur. Standardization enables automated, real-time settlement by establishing clear protocols for how value flows between parties. Customers see rewards credited instantly, merchants receive guaranteed payment, and banks maintain accurate accounting without manual reconciliation.

Key operational improvements include:

- Single integration point replaces dozens of custom merchant connections, reducing development and maintenance costs by 60 to 80%.

- Automated rule engines apply reward logic consistently, eliminating the errors that occur when humans manually process exceptions.

- Standardized data formats enable comprehensive analytics across all merchant partners, revealing optimization opportunities invisible in fragmented systems.

Scalability becomes exponential rather than linear under standardized frameworks. Adding a new merchant to a traditional program might require weeks of technical work and testing. With standardization, onboarding happens in hours because the merchant simply implements the common API specification. This speed advantage allows banks to expand merchant networks rapidly, creating more valuable programs that attract and retain customers. The universal purchasing power control layer demonstrates how standardization enables growth that would be impossible with custom integrations.

Pro Tip: When evaluating standardization platforms, prioritize those offering pre-built integrations with major payment networks and point-of-sale systems to minimize implementation time and technical risk.

The efficiency gains compound over time. As more merchants adopt standardized frameworks, network effects strengthen the entire ecosystem. Customers benefit from wider acceptance, merchants gain access to larger customer bases, and banks reduce per-transaction costs through economies of scale. This virtuous cycle explains why early adopters of standardization see competitive advantages that grow stronger as the market matures.

The financial benefits and ROI of standardized programs

Financial returns from standardized reward programs significantly outperform traditional fragmented approaches across multiple metrics. Industry benchmarks show that well-implemented standardized programs achieve 3x to 10x ROI within the first two years of operation. This performance stems from reduced operational costs, higher customer engagement, and improved redemption rates that drive incremental merchant revenue. Banks report that standardization cuts program administration costs by 40 to 60% while simultaneously increasing customer participation by 25 to 50%.

Retention improvements translate directly to bottom-line value. Standardized programs deliver 5 to 20% retention lift compared to non-standardized alternatives, and each percentage point of retention improvement can add millions in customer lifetime value for large institutions. When customers find rewards easy to earn and redeem across their preferred merchants, they consolidate more spending with the issuing bank. This behavioral shift increases interchange revenue, deepens customer relationships, and creates switching barriers that protect market share.

Payback periods for standardization investments prove remarkably short. Most programs reach breakeven within 6 to 18 months, making the business case straightforward even for risk-averse financial institutions. The rapid payback results from immediate operational savings that offset implementation costs while customer engagement builds gradually. Early returns come from reduced manual processing, fewer support tickets, and lower merchant integration expenses.

| Metric | Traditional Programs | Standardized Programs | Improvement |

|---|---|---|---|

| ROI Multiple | 1x to 3x | 3x to 10x | 200% to 333% |

| Retention Lift | 0% to 5% | 5% to 20% | 5 to 15 points |

| Payback Period | 24 to 36 months | 6 to 18 months | 50% to 75% faster |

| Admin Cost Reduction | Baseline | 40% to 60% lower | Significant savings |

The cost structure advantages become more pronounced at scale. Traditional programs face escalating integration and maintenance costs as merchant networks expand, while standardized programs exhibit near-constant marginal costs per additional merchant. This dynamic means larger programs see disproportionately better returns, creating competitive moats for institutions that standardize early. The universal purchasing power control layer architecture exemplifies how standardization enables profitable scaling that traditional approaches cannot match.

"Standardized reward programs transform loyalty from a cost center into a profit-generating customer engagement engine, with returns that improve as networks grow."

Operational efficiency gains free resources for strategic initiatives. When program managers spend less time troubleshooting technical issues and reconciling transactions, they can focus on optimizing reward structures, testing new merchant partnerships, and personalizing offers based on customer behavior. This shift from tactical execution to strategic management amplifies returns beyond the direct cost savings. Banks report that standardization enables A/B testing and rapid iteration that would be impossible with fragmented systems, leading to continuous performance improvements over time.

Navigating regulatory pressures and industry nuances

Regulatory changes are accelerating the shift toward standardized merchant rewards as financial institutions adapt to new interchange rules and settlement requirements. The recent Visa and Mastercard settlement agreements introduce interchange cuts and merchant flexibility provisions that fundamentally alter reward economics. Banks can no longer rely on high interchange fees to fund generous reward programs, forcing a pivot toward merchant-funded models that require standardized frameworks for efficient administration. Non-compliance with these new requirements risks higher processing costs and competitive disadvantage.

Visa's Commercial Enhanced Data Program (CEDP) illustrates the complexity of modern compliance requirements. The program mandates standardized enhanced data submission for commercial card transactions to qualify for lower interchange rates. Merchants and banks that fail to meet CEDP specifications face penalty rates that can exceed standard consumer card interchange. This regulatory pressure creates strong financial incentives for standardization, as only unified systems can reliably capture and transmit the required data elements across diverse merchant environments.

The regulatory landscape also highlights potential risks that require balanced program design. Research reveals that interchange-funded rewards redistribute $15B annually from less sophisticated cardholders to savvy users who maximize rewards. This wealth transfer raises fairness concerns and regulatory scrutiny, particularly as consumer advocacy groups push for more transparent fee structures. Standardized merchant-funded programs address these concerns by shifting reward costs to merchants who benefit directly from increased sales, creating a more equitable model that aligns incentives properly.

Key regulatory considerations include:

- Interchange rate qualification requires standardized data formats and submission protocols that fragmented systems cannot deliver consistently.

- Settlement timeline requirements mandate real-time or near-real-time processing capabilities only available through standardized platforms.

- Consumer protection regulations increasingly demand transparent reward terms and reliable redemption processes that standardization facilitates.

| Regulatory Driver | Impact on Programs | Standardization Benefit |

|---|---|---|

| Interchange caps | Reduces funding for bank-funded rewards | Enables merchant-funded alternatives |

| Enhanced data requirements | Increases compliance complexity | Automates data capture and submission |

| Settlement acceleration | Demands real-time processing | Provides built-in real-time capabilities |

| Transparency mandates | Requires clear reward terms | Ensures consistent customer communication |

Program managers must also consider industry-specific nuances when implementing standardization. Retail merchants face different regulatory requirements than travel providers or financial services merchants. Healthcare and government sectors impose additional data security and privacy constraints. A robust standardized platform accommodates these variations through configurable rule sets while maintaining core interoperability. This flexibility ensures compliance across diverse merchant categories without sacrificing the efficiency gains that standardization provides.

Pro Tip: Build regulatory compliance reviews into your standardization roadmap from day one, as retrofitting compliance into existing programs costs significantly more than designing it in from the start.

The regulatory trajectory points clearly toward continued pressure for standardization. As payment networks evolve and consumer protection frameworks strengthen, financial institutions that have already standardized their reward programs will adapt more quickly and cost-effectively than those maintaining fragmented legacy systems. This regulatory advantage compounds the operational and financial benefits, making standardization increasingly essential for competitive survival in the merchant rewards space.

Explore solutions for standardized merchant rewards

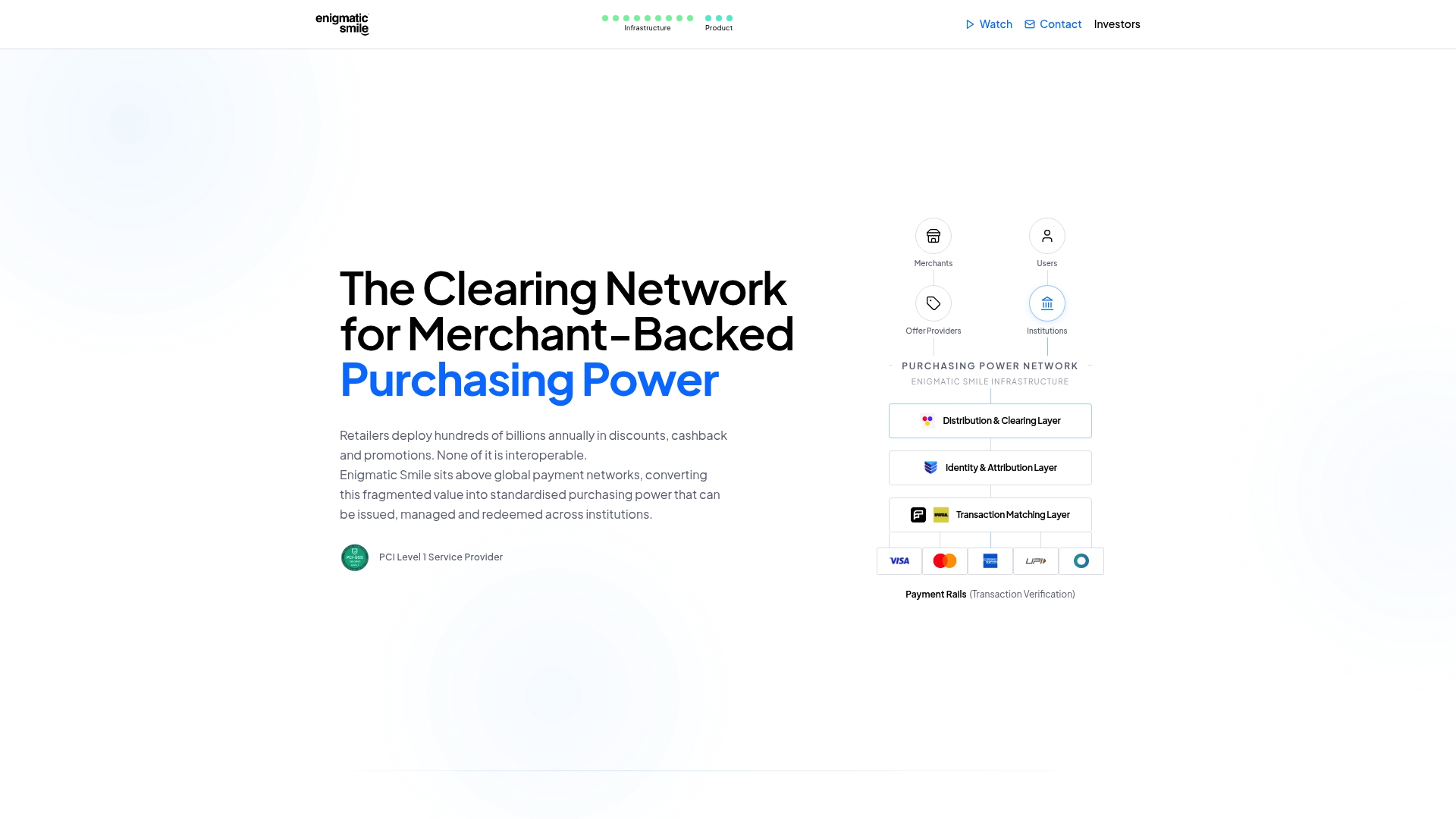

Financial institutions seeking to implement standardized merchant rewards need platforms that address the challenges outlined throughout this analysis while delivering measurable operational improvements. The Enigmatic Smile platform provides a modern solution by sitting above global payment networks and converting fragmented promotional value into standardized purchasing power. This architecture enables banks and loyalty programs to manage reward offers across hundreds or thousands of merchants through a single integration point, eliminating the custom development that traditionally consumes months of technical resources.

The platform automates critical processes that plague non-standardized programs, from campaign setup and eligibility verification to real-time redemption and multi-party settlement. Program managers gain unified dashboards that provide visibility across their entire merchant network, revealing optimization opportunities and performance trends impossible to detect in fragmented systems. The merchant management automation capabilities reduce administrative burden by 50 to 70%, freeing teams to focus on strategic initiatives rather than operational firefighting. For institutions ready to transform their reward programs from cost centers into engagement engines, exploring how a purchase control layer standardizes and scales merchant-backed purchasing power represents a practical next step toward greater efficiency and stronger customer relationships.

Frequently asked questions about standardizing merchant rewards

What are the primary benefits of standardizing merchant rewards?

Standardization delivers three core benefits: operational efficiency through unified APIs and automation, financial returns with 3x to 10x ROI and faster payback periods, and improved customer engagement via seamless cross-merchant experiences. These advantages compound over time as network effects strengthen.

How does standardization improve customer engagement?

Standardized programs reduce the confusion created by fragmented reward systems, making it easier for customers to understand how to earn and redeem benefits across merchants. This clarity drives 5 to 20% higher retention rates and increases program participation by eliminating friction from the reward experience.

Are there risks associated with interchange-funded rewards?

Yes, interchange-funded programs can redistribute wealth from less sophisticated cardholders to savvy users who maximize rewards, creating fairness concerns and regulatory scrutiny. Merchant-funded standardized programs address these risks by shifting costs to merchants who benefit directly from increased sales.

How do new regulations impact merchant rewards programs?

Recent interchange caps and enhanced data requirements from Visa and Mastercard push institutions toward standardized systems that can efficiently manage merchant-funded rewards and automate compliance. Non-compliance with programs like Visa CEDP results in higher processing costs that erode program economics.

What technical capabilities should standardized platforms provide?

Look for unified API layers that eliminate custom merchant integrations, real-time settlement capabilities for instant reward delivery, automated rule engines that apply reward logic consistently, and comprehensive analytics that reveal optimization opportunities across your entire merchant network.